Liquidity outcomes in private credit are largely determined at the point of sale, where fund structure, redemption terms, and investor expectations are initially set.

Not all evergreen vehicles are the same. Differences across public BDCs, non-traded BDCs, perpetual private BDCs, and interval funds meaningfully impact liquidity, governance, and investor experience.

When liquidity challenges arise, they often reflect structural design and communication gaps rather than underlying credit performance.

When a private credit fund limits redemptions, the headlines can be unforgiving. Investors feel trapped, and the manager absorbs blame for a problem that began long before the first redemption request was submitted, at the point of sale. In this article, we explain how private credit fund structures actually work, why redemption limits exist, who they protect, and what a realistic liquidity timeline looks like.

Private credit is often offered in a wide range of fund vehicles with meaningfully different liquidity profiles and regulatory frameworks. Treating them as interchangeable is the industry’s first and most costly mistake.

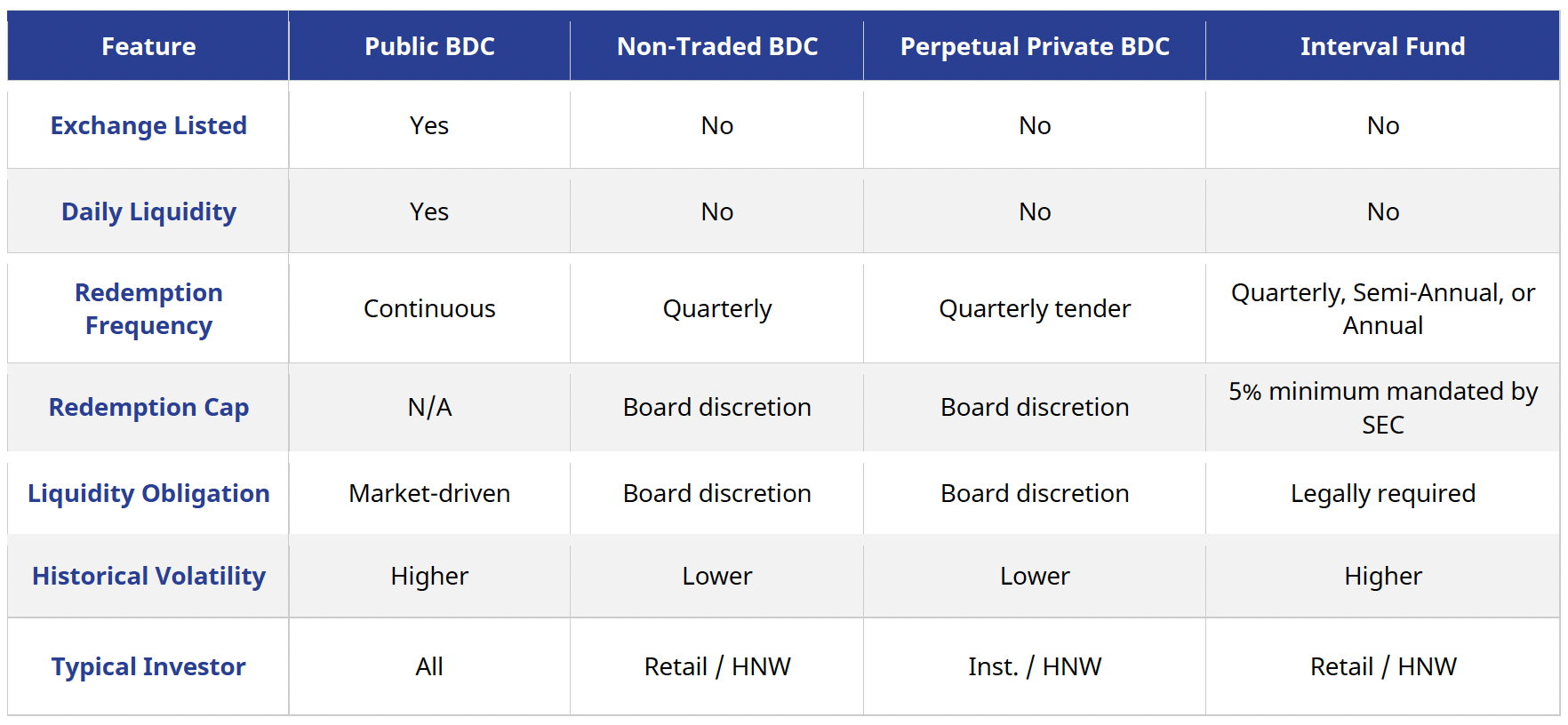

Publicly Traded BDCs

Listed on NYSE or NASDAQ, these offer genuine daily liquidity. The trade-off: market price is driven by both investor sentiment and portfolio performance. Discounts to NAV are common, especially in risk-off environments. Best suited for investors who need flexibility and accept mark-to-market volatility.

Non-Traded BDCs

SEC-registered, not exchange-listed. Quarterly redemption windows, typically capped at 5% of NAV per quarter, but these limits are subject to Board discretion, not regulatory mandate. Stable NAV orientation.

Perpetual Private BDCs

The most misunderstood structure. Built for institutional and sophisticated investors, including Accredited Investors and Qualified Purchasers, with elevated minimums and access requirements. No fixed end date. Liquidity is provided through periodic tender offers at the discretion of the Board.

Interval Funds

A mandated exception within private credit structures, interval funds are registered under the Investment Company Act and governed by Rule 23c-3. Unlike non-traded or perpetual private BDCs, they are legally required to repurchase a minimum of 5% and no more than 25% of outstanding shares. This is not Board discretion. Rather, it is a regulatory floor the fund cannot waive without SEC relief. It makes interval funds the most appropriate structure for retail investors who need a contractual baseline of periodic liquidity.

Structure Comparison

The root cause of most investor dissatisfaction with private credit was not structure failure. It was suitability failure at the point of sale.

Before any allocation, advisors must answer honestly:

The yield on private credit is partially compensation for illiquidity. If an investor is unwilling to accept the illiquidity, they are not entitled to the yield premium.

Private credit assets such as direct loans, mezzanine instruments, structured credit do not trade on exchanges. Selling them quickly means accepting unfavorable pricing. A Fund Manager that promises full liquidity on illiquid assets is not offering a feature. It is creating a liability mismatch that will harm investors when it matters most.

Redemption limits are in place to avoid a scenario where early investors exit at full value while the fund is forced to sell assets at unfavorable prices, leaving remaining investors to absorb the impact. By capping redemption volume, limits ensure no cohort is advantaged at the expense of another. When requests exceed the quarterly cap, redemptions are handled on a pro rata basis so each investor receives a proportional share, without preferential treatment.

For non-traded and perpetual private BDCs, the Board of Directors holds broad discretion over redemption policy, including the authority to reduce or increase caps or suspend redemptions temporarily. A Board that limits redemptions in a dislocated credit market is protecting remaining investors from a forced liquidation at the worst possible time. Interval funds, by contrast, cannot exercise this discretion at the floor. The 5% minimum mandate is legally binding under Rule 23c-3.

The growth of non-traded and perpetual private BDCs over the past years was fueled by yield-seeking investors and aggressive distribution. In that environment, education became a casualty. Wholesalers led with headline yield and monthly distributions. The liquidity discussion became a compliance disclosure that was signed but not understood.

When concerns around software exposure, alongside elevated redemption requests at Blue Owl’s OBDC II surfaced in the news, many investors sought liquidity across evergreen products and, in the process, discovered for the first time that redemption was not guaranteed. The frustration was understandable. The structure, however, was not the problem.

To help put this into context, the table below outlines how these structures typically operate in practice. Keep in mind, it is not a guarantee, but rather a planning framework.

Think of it like a CD: it does not penalize you for having a maturity date. It simply requires you to plan around it. Private credit funds require the same discipline.

Private credit itself has not changed, but expectations around it often have. Redemption limits are built into the structure to help preserve portfolio integrity and treat investors equitably during periods of stress. The interval fund’s mandated quarterly floor establishes a regulatory baseline of access. And the Board’s discretion in non-traded and perpetual vehicles is a fiduciary tool used to manage liquidity in the best interest of investors.

What drove the headlines was not the structure, it was what got lost in the conversation at the point of sale. For advisors, the liquidity discussion cannot be an afterthought. Instead, it needs to be part of setting expectations up front with the client. That means matching the structure to the client’s actual time horizon, documenting the conversation, and leading with the constraint before the yield.

For investors who approach this asset class with a clear understanding of the time horizon, redemption limits are not the issue. They are simply part of how the structure is designed to help protect capital when the market turns.

We welcome a conversation. Please contact invest@pennantpark.com or the professionals listed below.

PennantPark was founded in 2007 as an independent middle market credit platform. The firm was founded by Art Penn, a private credit industry veteran that previously co-founded Apollo Investment Management. We have invested over $27 billion across multiple economic and credit cycles since inception, and we manage $10 billion in AUM today.[i] PennantPark serves a broad range of sophisticated investors with product offerings that include business development companies, private capital funds, joint ventures, and other specialized funds.

Our highly experienced team primarily invests in the core middle market, targeting companies with earnings of $10 million to $50 million. These mid-sized companies are often overlooked by banks and large investment managers, resulting in senior secured loans that generally feature higher yields, lower leverage, and stronger lender protections when compared to the upper middle market and broadly syndicated loans. We focus on five key industry verticals where we have the most expertise and experience. These industries include healthcare, government services, business services, consumer, and software & technology.

[i] Assets under management (“AUM”) is defined as the sum of gross asset values, unfunded commitments, joint ventures and undrawn available leverage for active funds as of 12/31/2025. Invested capital represents the cumulative sum of capital invested across the PennantPark platform since inception through 12/31/2025. Figures are rounded to the nearest billion.

©2026 PennantPark Investment Advisers, LLC (‘PennantPark’) is an investment adviser registered with the US Securities and Exchange Commission (‘SEC’). Registration is not an endorsement by the SEC nor an indication of any specific level of skill. The material included in this document is intended for informational purposes only. Products or services referenced in this document may not be licensed in all jurisdictions, and unless otherwise indicated, no regulator or government authority has reviewed this document, or the merits of the products and services referenced herein. This document and the information contained herein has been made available in accordance with the restrictions and/or limitations implemented by applicable laws and regulations.

In considering the past performance information contained herein, recipients should bear in mind that past performance is not a guarantee, projection or prediction and it is not a guarantee or indication of future results. Invested capital is at risk. There can be no assurance that any product or service referenced herein will achieve comparable results, or that they will be able to implement their investment strategies or achieve their investment objectives.

An investment with PennantPark in any advised fund is suitable only for sophisticated investors and requires the financial ability and willingness to accept the risks and lack of liquidity that are characteristic of an investment in such funds. Investors must be prepared to bear such risks for an extended period. There can be no assurance that any investment will be profitable, not lose money, or achieve the other intended purposes for which they are made. Investing with PennantPark will expose the investor to various risks including, but not limed to, the following: 1) Lack of Liquidity Risks including lack of permitted withdrawals, lack of secondary market, and lack of transferability 2) Interest Rate Volatility Risks 3) Use of Leverage Risks 4) Securitization Risks 5) Credit Market Disruption Risks 6) Investing within a Highly Competitive Market Risks 7) Default by Borrowers Risks 8) Recovery on Bad Debt Risks including cost of recovery 9) International Market Exposure Risks 10) Inflation and Deflation Exposure Risks. This is not intended to be a complete description of the risks of investing with PennantPark.

The information contained here does not constitute, and is not intended to constitute, an offer of securities and accordingly should not be construed as such. Any such offering of a Pennant Park fund can be made only at the time a qualified offeree receives a confidential private offering memorandum, prospectus and/or other operative documents which contain significant details with respect to risks and which should be carefully read. All information contained in this presentation is qualified in its entirety by each fund’s operative documents. Investors should rely on their own examination of the potential risks and rewards. The firm brochure (Form ADV 2A) is available online at www.adviserinfo.sec.gov or upon request and also discusses these and other important risk factors and considerations that should be carefully evaluated before making an investment. Information in this document does not constitute legal, tax, or investment advice. Before acting on any information in this document, current and prospective investors should inform themselves of and observe all applicable laws, rules and regulations of any relevant jurisdictions or obtain independent tax, legal, or investment advice.

This document may not be reproduced and may not be redistributed to any party without prior written consent. Statements in this document are made as of the date hereof unless stated otherwise herein, and neither the delivery of this document at any time, nor any sale hereunder, shall under any circumstances create an implication that the information contained herein is correct as of any time after such date. Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. PennantPark believes that such information is accurate and that the sources from which it has been obtained are reliable. PennantPark cannot guarantee the accuracy of such information, however, and has not independently verified the assumptions on which such information is based. Certain statements contained in this document, including without limitation, statements containing the words “believes,” “anticipates,” “intends,” “expects,” and words of similar import constitute “forward looking statements.” Additionally, any forecasts and estimates provided herein are forward-looking statements. Such statements and other forward-looking statements are based on available information and the views of PennantPark as of the date hereof. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results and events may differ materially from those in any forward-looking statements. Further, any opinions or analysis expressed are the current opinions or analysis of PennantPark only, are not guaranteed, and may be subject to change, without notice. There is no undertaking to update any of the information in this document. No person has been authorized in connection with this document to give any information or to make any representations other than as contained in this document and, if given or made, such information or representation must not be relied upon as having been authorized by PennantPark or PennantPark’s affiliates.